.svg)

Introduction

There's been a sharp rise in the percentage of respondent banks reporting it is 'difficult or impossible' to access US currency in recent years. Between 2013 and 2019, this rose to 19% according to the European Bank for Reconstruction & Development (ERBD).

Even with increased revenue avenues for correspondent banks, minimal training requirements, and low barriers to entry when entering new markets, why is establishing relationships with respondent banks still considered high risk for financial institutions (FIs)?

In this article, we examine why respondent banks are facing difficulties when it comes to anti-money laundering (AML) compliance and how standardised benchmarking would prevent unnecessary de-risking on behalf of FIs, opening up new opportunities for correspondent and respondent banks alike.

Current perceptions of correspondent banking

Correspondent banks often must rely on the risk policies implemented by their respondent partners - each one unique to the bank they enter into business with. Due to this, correspondent banking has increasingly been viewed as high risk in recent years, stemming from the long-term impact of the financial crash and exacerbated by inabilities of influential banks in recent years to prevent money laundering scandals associated with correspondent banking failures, where respondent banks’ risk policies have not been stringent enough.

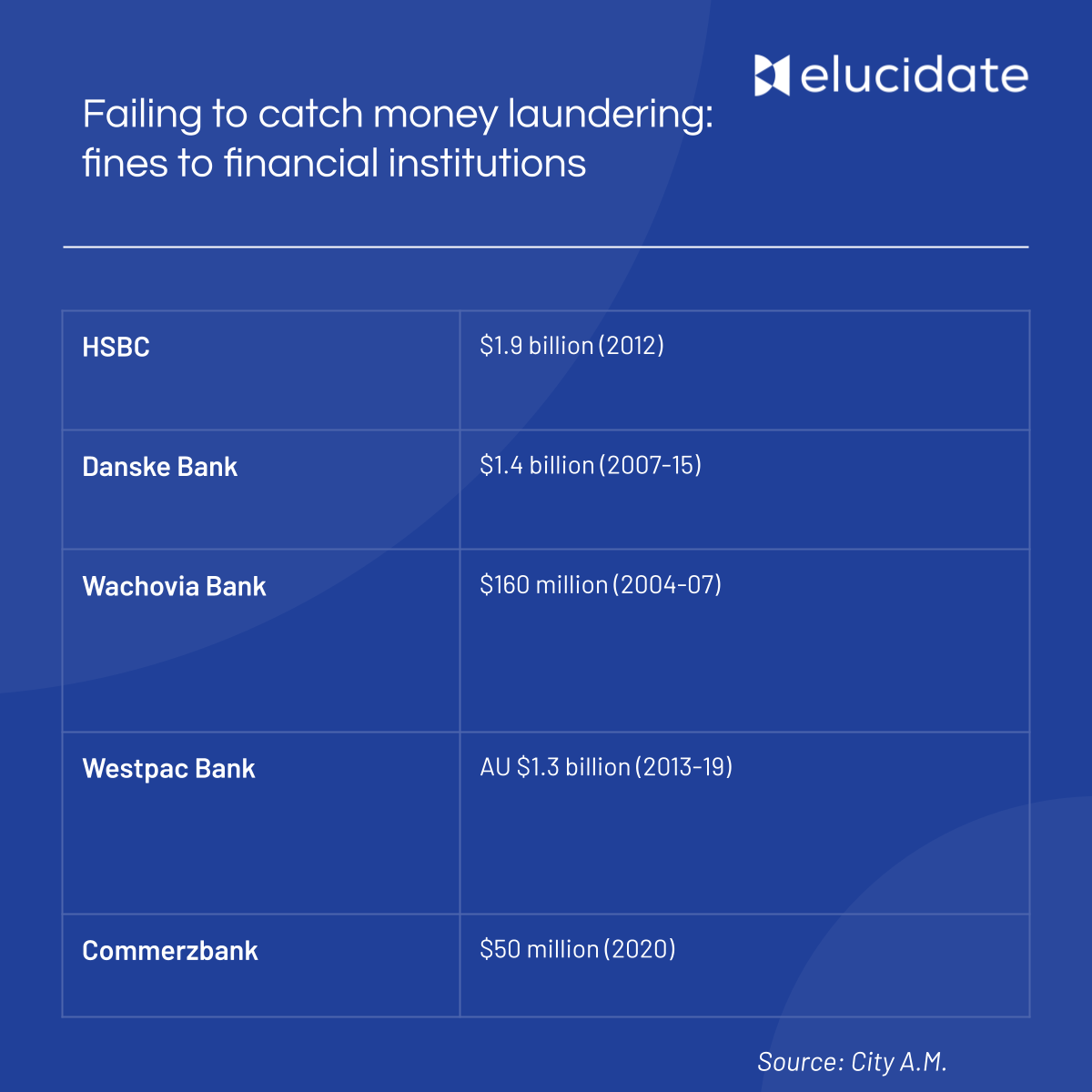

For example, Dankse Bank was embroiled in a $200 billion money laundering scandal between 2017-2018 and more recently this year, Credit Suisse failed to detect the laundering of 146 million Swiss Francs. The former incident led to a 60% cut in Deutsche Bank's correspondent banking services. The reputational damage of these has impacted correspondent banking as a process, leading to a wave of de-risking across financial markets (you can read more about this here), cutting off much needed resources to distressed or emerging markets.

The COVID-19 pandemic has only increased the level of stress that respondent banks in emerging markets have experienced in their correspondent banking relationships; around 10% of banks reported their access to the US payment system had been severely limited or even completely lost due to the withdrawal of correspondent banks.

These trends clearly undermine efforts that respondent banks might otherwise take to improve controls and shore up their own financial crime risk management; with the reputation of the market against them in any future business scenarios. In addition, it may encourage a culture of compliance with correspondent bank risk standards regardless of what a respondent institution's own risk-based approach should look like.

Why correspondent banking is crucial to local markets

However, despite the perception of correspondent banking declining in recent years, its importance to the markets it serves hasn’t.

Respondent banks play a crucial role in their local economies, especially in emerging markets. Having access to international finance, as well as the ability to make and receive cross-border payments for customers, is necessary for their business and wider economies. Remittances are also sent frequently by foreign workers to their families in their home countries to supplement their income.

Access to global financial markets is a known driver of financial inclusion, fuelling economic growth and development the world over. So why is it so difficult for respondent banks to gain the trust of correspondent banking partners, and prevent hasty de-risking?

How de-risking impacts respondent banks

By de-risking, many correspondent banks avoid providing services to clients who fall into certain risk categories - this often means leaving markets and regions altogether and preventing respondent banks from accessing crucial financial ecosystems. Sadly, de-risking has the detrimental effect of preventing humanitarian agencies from providing much needed funds for refugees and disaster victims in these regions. Additionally, de-risking shifts crime risks to the fringes of the industry, where it becomes harder to monitor money movements once transactions move from formal to illicit channels.

Currently, respondents have little opportunity to negotiate the decisions made against them due to the lack of transparency regarding the risk assessments made of their organisations.

De-risking has an impact on corresponding banks - although it may prevent potential risks, de-risking without a holistic evaluation prohibits long-term, lucrative partner relationships and revenue opportunities in emerging markets.

Why unnecessary de-risking happens

Correspondent banking plays a crucial role in the smooth functioning of large developed economies, as well as emerging economies and the broader financial inclusion agenda, so a solution that encourages full transparency, effective dialogue between the parties, and keeps financial markets open to everyone is clearly beneficial for everyone.

Because of a lack of benchmarking and transparency, correspondent banks are forced to de-risk far more abruptly. Each FI uses their own processes and systems to determine whether a prospective respondent bank is low or high risk and what the definition and outcome of ‘risk’ might be. However, what’s missing is a common benchmark - one where all FIs in the network are evaluated comparatively, and not penalised based solely on geographic or political factors but assessed based on a range of nuanced criteria.

At present, blanket de-risking of respondent banks is based on subjective risk assessments, a business model detached from financial crime risk management - which is treated as an issue of strict compliance - as well as onerous due diligence processes, even when financial crime risk is low. A lack of objective data insights informing AML programmes can prevent decisions being accurate and fair to respondent banks and potential partners.

Beyond the tactical, day-to-day requirements of enabling legitimate correspondent banking activity to continue, there is also a larger strategic issue around the advantages for both correspondent and respondent banks in adopting an industry benchmarking approach to financial crime risk. Currently correspondent relationships are largely managed on a bilateral basis, with important decisions around financial crime risk often being made on a variable and subjective understanding of risk.

The solution? A standardised benchmark

Financial crime risk management needs the discipline, methodology and measurement capabilities that underpin other types of risk management. This then opens the door to the possibility of pricing financial crime risk into products and services, managing or spreading the risk through the use of financial crime derivatives and contributing to assessments of Environmental, Social and Governance (ESG) factors too.

Therefore, greater transparency is highly desirable to enable corresponding banks to make more informed decisions about respondent banks that are more in line with their risk appetites; allowing a collaborative relationship between both correspondent and respondent, where remedial action on behalf of respondents, or changes to pricing to reflect risk are prioritised over exiting markets and de-risking. This also ensures respondents know how they can improve, and creates trust between all parties. By clearly raising the standards FIs are forced to operate against - every institution in the network would benefit.

Assess institutional risk with Elucidate

The Elucidate’s platform provides a comprehensive view of a bank’s own risk, as well as that of its counterparties. With our platform, nine scores are generated based on high quality data across a range of risk themes, allowing accurate and fair evaluations and comparisons of institutions across a range of risk categories.

With Elucidate, banks can visualise their risk across 9 risk categories:

- Sanctions

- Transactional activity

- Organisational reputation

- Employee conduct

- Bribery and corruption

- Geographic footprint

- Customer portfolio

- Products and channels

- Governance framework

According to the results of this, banks are not necessarily required to de risk, since they can identify areas of risk and allocate resources accordingly when operating in high-growth or distressed regions.To learn more about this solution, book a demo today with one of our team.