Introduction

Correspondent banking is when one bank (the correspondent) provides services to another bank (the respondent); often this involves the facilitation of cross-border payments by one institution on behalf of another. For emerging markets, it is a crucial tool for accessing global networks, allowing for international finance and ensuring proper functioning of global financial systems.

However, over the last few years large banking scandals - such as recently, with Danske Bank pleading guilty to fraud for facilitating money laundering - have contributed to a negative perception of correspondent banking. Additionally, respondents encounter systemic limitations, such as a lack of clarity on how data can be gathered based on correspondent risk appetite, a lack of processes for holistic risk analysis, and difficulties automating transaction monitoring and client assessments. For this reason, developing remediation strategies to build new correspondent banking partners is challenging.

The crucial role of relationships with correspondent banks makes it so important to understand some of the limitations of the current correspondent banking system that are driving these changes in use as the more you understand the risks and limitations of the correspondent banking system, the better your chances are of mitigating concerns of potential banking partners and accessing vital global financial services.

In this article, we discuss the limitations of the current correspondent banking system. By understanding your own bank's profile with the right tools, we will help you stay ahead of your competitors when sourcing and building relationships with your banking partners.

The limitations of the current correspondent banking system

As each correspondent bank has varying degrees of risk appetite and different procedures for evaluating respondents, often this has given rise to varying levels of client due diligence, allowing multiple cases of money laundering and financial crime to slip through the net during financial crime risk management and evaluations within notable institutions.

For example, between 2007 and 2015, the Estonian arm of Danske Bank was found to be responsible for the facilitation of $236 billion of illicit transactions. In 2013, six years after the first transactions were processed, JP Morgan ended working with Danske Bank citing concerns over these illegitimate funds. Although Deutsche Bank decided to continue working with Danske Bank until 2015 - they scaled back their services by 60%.

This is indicative of the outcome of many of these kinds of scandals - where ultimately, unable to cope with the enormity of due diligence processes and in fear of being caught in similar circumstances, many correspondents opt to cut back services they offered to respondent banks across multiple jurisdictions, regions and markets.

The decline in correspondent banking relationships (which you can read more about here) has led to the biggest risk for respondent banks - being de-risked by existing correspondent banks and therefore losing correspondent services and the opportunity to service existing customers.

So, in this complex climate, how does your institution avoid a loss of services to continue to serve your customers and generate new opportunities?

How to prevent loss of services

Losing access to correspondent banking services can have a significant impact on the functioning of a respondent bank, directly impacting the ability of the bank to operate in a jurisdiction and serve its customer needs.

To avoid loss of service, a thorough and continuous risk assessment of your internal banking is needed, to prevent de-risking. The appropriate due diligence on your prospective correspondent bank is also important to ensure you are the right fit for your partner institution. You can read more about the steps to doing this here.

Before entering any new partnerships you must conduct thorough internal due diligence to make sure your institution is ready to enter new partnerships and will be able to satisfy the risk appetite of your correspondent bank.

The Australian Government for example has a useful guide for what to consider in due diligence of your correspondent banking partner. These include as an overview:

Ownership structures

- If your bank is publicly owned, the shares must be traded on a market or exchanged in a location with a robust regulatory regime

- If your bank is privately owned, the identity of the ultimate beneficial owners must be clear and noted

- The location, structure and experience of all board directors and executives must be documented, including any status as a politically exposed person

Business processes

- The correspondent bank must be notified of all products, services, delivery types and customer types

- The types of transactions carried out as part of the correspondent banking relationship must be documented

Relationships with foreign countries

- The AML/CFT systems and controls must be in place for the ultimate parent company

- The quality of the AML/CFT laws, regulations and supervision in the jurisdiction of residence for the bank is essential

- If your bank is a subsidiary of a large group, robust AML/ CFT controls to FATF or equivalent standards should be implemented

Company standing reputation

- The compliance history of the organisation will be an important part of any de-risking decisions for the correspondent bank

- If your organisation has been subject to investigation or regulatory action in relation to AML/CFT obligations, this will be considered a red flag

By following these steps, you can make it easier for correspondent banks to see viability in your institution's role as a respondent.

Understanding your bank to overcome correspondent banking challenges

With the challenges outlined in preventing loss of service, having a holistic view of your bank and subsequent risk exposure will allow you to effectively mitigate risks and assure your correspondent partners that you are on top of the threat landscape.

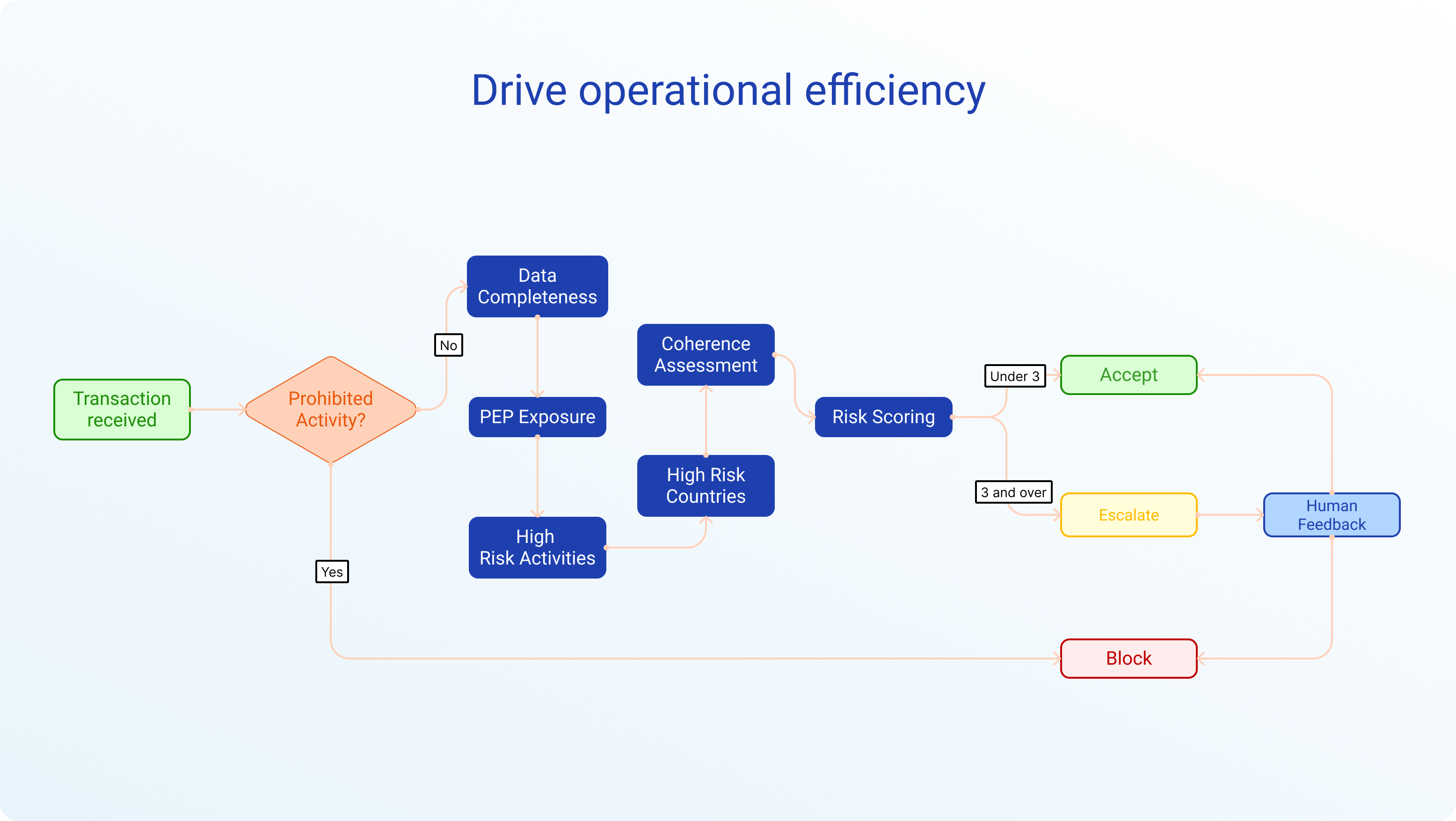

Understanding your internal data and creating a complete data picture of your risk exposure is the key element in this, particularly if you operate in a high-risk jurisdiction. To do this, effective transaction monitoring is needed to process the large volumes of data, discard false positive results and address any suspicious transactions. Transaction monitoring can be a significant resource spend for most financial institutions, particularly with the global increase in digital payments.

According to a report by Europol, around 10% of suspicious transaction reports filed by financial services firms lead to further investigation by regulatory authorities. Having the appropriate tools in place, rather than relying on manual intervention and analysis will therefore support the streamlining and automation of the process and ensure you can provide accurate information to your correspondent bank.

Artificial intelligence and machine learning techniques can offer improved efficiency in this space, with tools offering up to a 50% reduction in false positive results.

Increasing the levels of automation within the bank can free up resources for the further investigation of financial crime risks. As resources are allocated to investigate suspicious activity, the data generated can be used to train your transaction monitoring models and continuously improve the algorithms used within the bank for detecting financial crime. Investing in technology can be transformative for your organisation, but it requires cultural buy-in from senior management.

Without the help of tools, satisfying your correspondent partner can be a near-impossible challenge and the likelihood of loss of service becomes increasingly probable. The global investment landscape in AI solutions has increased year on year, with annual venture capital investment for US based AI startups seeing a six fold increase from 2000-2017.

In 2017, over £238m of venture capital funding was poured into RegTech (regulatory technology) firms in the first quarter alone, and this investment trend has continued, with an estimated $12bn investment in RegTech ventures in 2021. Given the growing popularity of such solutions, not using data and technology to power your conversations with correspondent partners will hinder any service discussions and be a clear barrier to forming an agreement. With the move towards digitisation, the need to invest and avoid being left behind by your competitors is more important than ever.